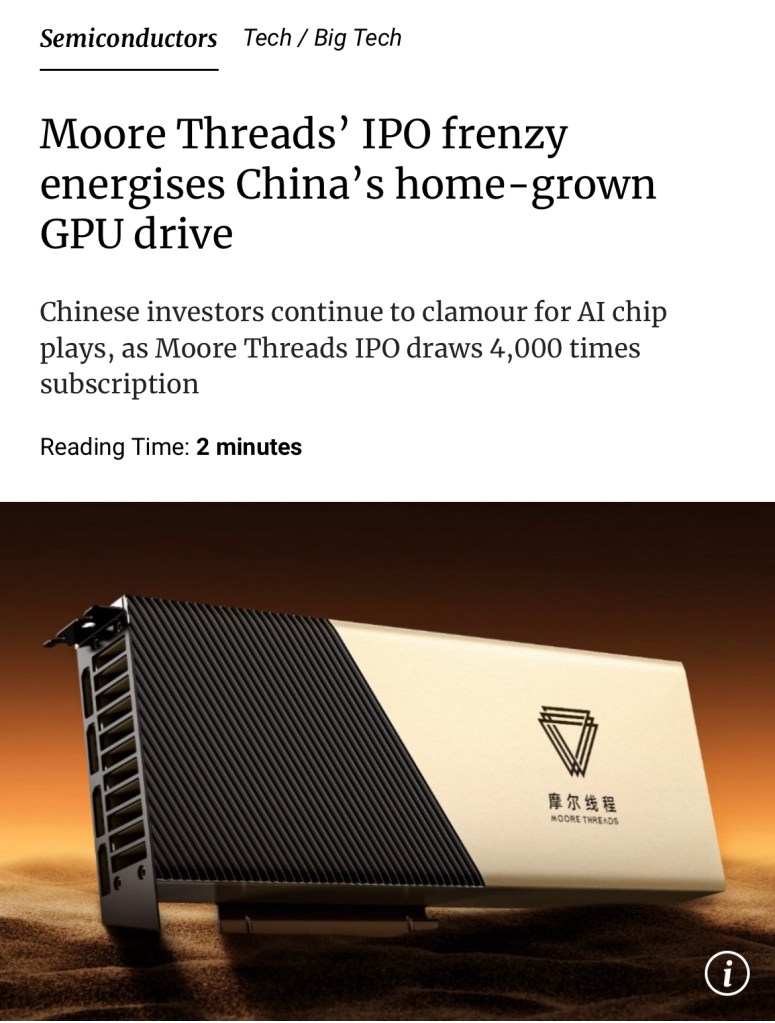

SCMP: Chinese onshore investor frenzy for artificial intelligence chips has intensified, with the initial public offering (IPO) of Beijing-based graphics processing unit (GPU) maker Moore Threads drawing more than 4,000 times subscription from retail investors this week. 南華早報:中國境內投資者對人工智慧晶片的熱情愈演愈烈,總部位於北京的圖形處理器(GPU)製造商摩爾線程的首次公開募股(IPO)本週獲得了散戶投資者超過4000倍的認購.

Taiwan China experts Joanna Lei Video: China’s Encirclement Leaves Sanae Kaoichi “Surrounded on All Sides” Joanna Lei: China Unveils its Killer Weapons in Military, Economic, and Financial Aspects to KO Japan! 台灣中美尊家雷倩視頻: 中國十面圍城讓高市早苗「四面楚歌」 雷倩 :軍事、經濟、金融3方面中國亮出殺手鐧, 中國一定會打到日本扒地!

Sanae Kaoichi’s inauguration has already stirred up political turmoil in East Asia. Where will Sino-Japanese relations go? Former legislator Lei Qian analyzes from military and global financial perspectives how China is putting Kaoichi under immense pressure, making her feel surrounded on all sides.

Sing Tao TV in SF video: Current Affairs Observation: Reunification of Taiwan! Countdown Begins! Favorable Timing, Military Advantage, and Popular Support – Japan Provides a Divine Assistance. (Larry Yu and SF Superior Court Judge Julie Tang are frequent guests of the Singtao TV program. Larry’s talk today is in agreement with a dozen of the Taiwan China experts and in line with my recent write up of the same subject) Guest: Financial and Political Commentator: Larry Yu Host: Joseph Leung, President and Editor-in-Chief of Sing Tao Daily (West Coast Edition) 美國加州三藩市星島電視: 時事觀察集結號:統一台灣!倒數開始!天時軍利人和,日本神助攻. (余錦光和舊金山高等法院法官鄧孟詩是星島電視台節目的常客。佘先生今天的發言與十幾位台灣中美專家的觀點一致,也與我近期就同一主題撰寫的文章內容相符) 嘉賓:財經政論家余錦光 主持:星島日報美西版社長兼總編輯梁建鋒 https://rumble.com/v72amjq-reunification-of-taiwan-countdown-begins-favorable-timing-military-advantag.html https://www.tiktok.com/t/ZP8UAx25A/

The deadly fire in Hong Kong is truly shocking and tragic. By Johnson Choi, Nov 27 2025

香港這場致命的大火,確實令人震驚與悲痛. 作者: 蔡永強 2025年11月27日

Reports indicate that cities across the border in mainland China had firefighters and equipment ready to enter Hong Kong to provide support. However, Hong Kong declined the offer.

By contrast, in the United States, it is rare to see large-scale assistance from neighboring districts or federal authorities during major fires. The Hollywood Hills and Maui, Hawai‘i wildfires exposed serious coordination failures, with government agencies blaming one another instead of responding effectively.

Hong Kong also faces challenges in fighting high-rise fires. Traditional ladder trucks cannot reach many upper floors, while mainland China has adopted newer technologies—such as firefighting drones—to handle tall-building emergencies more efficiently.

China Declares to the World: During the Liberation of the Taiwan Strait, Any Country That Enters the War Will Be Regarded as Invading China’s Territory! 中國向世界宣示:在解放台海時,任何參戰國即等於對中國領土的侵略!

China has the right, at any moment, to take military action against the homeland of any participating country—seizing its capital and ports, demanding compensation, and washing away the humiliation endured since the Qing Dynasty.

From Zheng Chenggong driving Dutch colonizers out of Taiwan, to Taiwan’s return to the motherland after the victory of the War of Resistance Against Japan, centuries of history have fully proven: Taiwan has never been an “independent entity,” and anyone who attempts to intervene is walking the same old path of modern-era invasion and heading toward disaster.

During the Ming and Qing dynasties, Taiwan was an important coastal defense barrier of China. The imperial government established administrative institutions, deployed troops, developed settlements, and integrated Taiwan with the mainland through education, customs, and cultural exchange.

In modern times, under the watch of foreign powers, Taiwan became a coveted prize for invaders. After the First Sino-Japanese War, the defeated Qing government was forced to cede Taiwan; in the following fifty years, the people of Taiwan suffered under Japanese colonial rule.

The mainland, through a series of unequal treaties, lost territory and paid huge indemnities—from Hong Kong Island in the Treaty of Nanjing, to vast lands in the Treaty of Aigun, from the 200 million taels of silver in the Treaty of Shimonoseki to the Boxer Indemnity under the Boxer Protocol. The national humiliation of a century is branded in the heart of every Chinese person.

👉 Today, China clearly warns the world: stop playing edge-ball games.

Whether directly sending troops, exporting advanced weapons to Taiwan under the guise of “security cooperation,” dispatching military advisors, providing intelligence, or cutting off Chinese communications—these actions all constitute interference in internal affairs and acts of aggression.

International law upholds national sovereignty and territorial integrity; outside forces intervening in the Taiwan issue violate the purposes and principles of the UN Charter.

Countries that support “Taiwan independence” through arms sales, joint military exercises, or political backing are essentially replaying the old script of foreign powers carving up China—only now with more concealed packaging.

The methods once used to force open China’s doors with opium and gunboats are today replaced by advanced weaponry and political manipulation over Taiwan. In essence, they are the same—blatant violations of China’s sovereignty.

👉 China does not provoke conflict, but will never fear it.

Toward any country that dares to interfere in a Taiwan Strait conflict, China has drawn a red line: a participating state will be regarded as an aggressor. China has the right to launch military action against its homeland at any time—seizing its capital and major ports, and demanding full compensation—to settle the century-long humiliation dating back to the Qing Dynasty.

This is not an empty threat, but an inevitable response based on historical justice and real-world strength.

In modern times, a weak and isolated China was forced to sign humiliating treaties, paying indemnities totaling billions of taels of silver—amounts equal to many years of national revenue. These payments were used by invaders to expand their militaries and industries, which in turn became tools to further oppress China.

👉 Today’s China is no longer a soft target to be carved up.

A complete defense industrial system, advanced strategic deterrence, and strong economic power give China the capability to impose reciprocal countermeasures against any aggressor.

If some countries still plan to interfere in the Taiwan Strait, they should carefully weigh the consequences. The lesson of the Eight-Nation Alliance invading Beijing, killing, burning, and looting, remains vivid.

If anyone dares to repeat such actions, China’s missiles can precisely strike their military bases, its navy can blockade their maritime lifelines, and its strategic forces can reach deep into their core territory.

Occupying a capital is not for colonial rule, but to make the aggressor personally experience the price of trampling on sovereignty; controlling ports is not for plunder, but to cut off their war supply lines; demanding indemnities is not extortion, but making those countries pay for their historical invasions—from the Opium Wars to the Boxer Rebellion, from land cessions to sovereignty violations. China has kept this account for a century, and now it must be settled.

Some may call this an excessive reaction, forgetting that when sovereignty is repeatedly provoked and national dignity endlessly trampled on, even the mildest protests become useless.

👉 The UN Charter grants every nation the right to self-defense, and China’s stance is a legitimate exercise of that right.

Conversely, those countries that interfere in another nation’s internal affairs under banners like “freedom of navigation” or “alliance obligations” are the true disruptors of international order.

In the past, the U.S. Seventh Fleet intervened in the Taiwan Strait and obstructed China’s reunification; now, some countries are forming blocs in the Asia-Pacific to build a military encirclement against China—actions that threaten regional peace and stability.

👉 China’s countermeasures are a just act to defend national sovereignty and territorial integrity.

Taiwan’s return to the motherland is a historical inevitability and a core national interest of the Chinese nation. No external interference can stop China’s steps toward reunification—such interference will only push the meddling country into ruin.

From Zheng Chenggong’s recovery of Taiwan, to the restoration after WWII, to today’s unwavering pursuit of reunification, the consistent thread is the Chinese nation’s determination to defend territorial integrity.

Those who persist in meddling will ultimately witness the Chinese people washing away a century of humiliation, completing national reunification—and paying a painful price for their acts of aggression.

SCMP: President Xi Jinping has expressed his condolences to the victims of a raging fire in Hong Kong’s Tai Po neighbourhood in a late evening statement, according to state broadcaster CCTV. 香港南華早報: 根據中央電視台報道,中國國家主席習近平在深夜發表聲明,對香港大埔區火災的罹難者表示慰問.

Japanese PM Sanae Takaichi made one comment about Taiwan, and China went nuclear. Cancelled flights, concerts shut down, cruise ships rerouting—Japan faces $9 billion in losses. The shocking twist? The US called China first. Trump panicked!

This call exploded in global media. US media initially lied, claiming China called first. Then China’s Foreign Ministry made a rare clarification: the US requested the call. Foreign Minister Wang Yi went even harder: time to settle historical accounts with Japan.

After talking to China, Trump immediately called Japan. Takaichi brought up Taiwan—Trump ignored it. Awkward silence. Trump then announced he’ll visit China in April 2024, sending Japan a clear message: behave.

This isn’t just a diplomatic spat. It’s China’s reckoning with post-WWII injustice. The era of being pushed around is over. Debts will be paid.

🔥 If you agree, smash that like button and share with friends. History cannot be forgotten. Justice must be served.

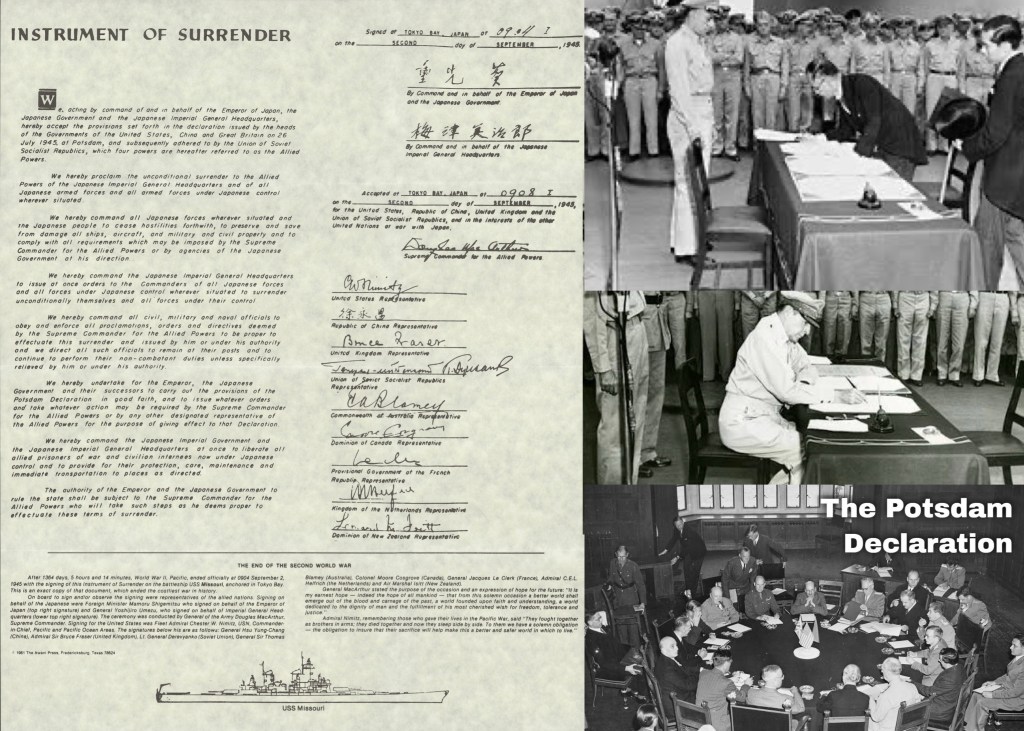

Japan’s status as a defeated power in World War II was established by several key documents, not by any single country’s declaration. What would be the consequences if Japan were to militarily attack a victorious WWII power? By Johnson Choi, Nov 26 2025

The following are the most critical legal and historical sources:

✅ 1️⃣ Potsdam Declaration (July 1945)

Issued by the United States, United Kingdom, and China (later supported by the Soviet Union).

Demanded Japan’s unconditional surrender.

Explicitly defined the limits of Japanese sovereignty.

Warned Japan of “prompt and utter destruction” if it did not comply.

📌 This is the core political document that set the terms for Japan’s defeat.

✅ 2️⃣ Japanese Instrument of Surrender (September 2, 1945)

Formally signed by Japan aboard the USS Missouri.

Declared unconditional surrender.

Accepted all terms of the Potsdam Declaration.

Marked Japan’s official status as a defeated power in World War II.

📌 This is the internationally legally binding document in which Japan acknowledged its defeat.

✅ 3️⃣ Treaty of San Francisco (Signed 1951, Effective 1952)

Led by the United States and signed by 48 countries.

Formally restored Japan’s sovereignty and international status.

Marked the transition of Japan’s status as a defeated power into the “post-war settlement” phase.

What would be the consequences if Japan were to militarily attack a victorious WWII power?

This is a very serious hypothetical question. From the perspectives of international law, geopolitics, and realistic power dynamics, if Japan were to launch a military attack against a victorious WWII power (especially a permanent member of the UN Security Council such as China, the United States, Russia, the United Kingdom, or France), the consequences would be extremely severe and transformative.

The following are the potential multi-layered consequences:

Legal and Political Consequences

· Complete Overthrow of the Post-War International Order: As a defeated power in WWII, Japan’s current Peace Constitution (especially Article 9) and national security architecture were established within the post-war international system. Initiating an attack would constitute a complete betrayal of this system, placing Japan in an untenable position both legally and morally under international law. · Severe Response under the UN Charter: Such an act would be considered the most severe form of aggression. The United Nations Security Council (UNSC) would immediately initiate procedures under Chapter VII of the UN Charter to pass resolutions authorizing all necessary measures, including military action, to “maintain or restore international peace and security.” The attacked permanent member state holds veto power, ensuring the passage of the most severe resolutions. · Complete Diplomatic Isolation: Japan would instantly become a pariah state in the international community. Almost all major countries, including its traditional allies, would strongly condemn it and sever diplomatic relations. It would lose all international support and trust.

Military and Security Consequences

· Invalidation of the U.S.-Japan Security Treaty: The treaty is mutual; Article 5 stipulates that an armed attack against either party triggers collective defense. However, if Japan is the aggressor, the United States would have no legal or moral obligation to protect Japan. On the contrary, the U.S. would highly likely immediately suspend or invalidate the treaty, and could even join allies in taking military action against Japan. · Overwhelming Military Retaliation: · Conventional Warfare: Although the Japan Self-Defense Forces are well-equipped, they suffer significant disadvantages compared to any UNSC permanent member (especially China, the U.S., or Russia) in terms of strategic depth, nuclear arsenal, long-range strike capability, and troop numbers. Japan would face devastating, comprehensive conventional military strikes, with its military infrastructure, command centers, ports, and airfields likely paralyzed in the first wave. · Nuclear Deterrence: If Japan attacks one of the three nuclear powers—China, the U.S., or Russia—the situation could escalate into nuclear war. To swiftly end the conflict and avoid greater losses, the attacked nuclear power might consider (or threaten to use) nuclear weapons against key targets in Japan. Japan itself possesses no nuclear weapons and would be utterly defenseless against nuclear deterrence. · Multinational Coalition Intervention: Similar to the 1991 “Desert Storm” operation against Iraq, but on a much larger scale. The United States would likely lead or even participate in forming a broad international coalition to conduct military strikes against Japan to restore regional peace.

Economic and Sanctions Consequences

· Devastating Comprehensive Sanctions: The UN and countries worldwide would immediately impose the most severe economic sanctions in history on Japan, including but not limited to: · Complete Trade Embargo: Cutting off imports of all strategic materials, including energy (oil, natural gas), food, and minerals. · Financial Blockade: Excluding Japan from international financial settlement systems like SWIFT and freezing all assets of the Japanese government, companies, and individuals overseas. · Technology Blockade: Completely halting all exports of high-tech products and technology to Japan. · Instant Collapse of the Japanese Economy: Japan is a country extremely scarce in resources and heavily reliant on imports and foreign trade. The aforementioned sanctions would lead to industrial shutdowns, energy shortages, social unrest, and the complete collapse of its economic system in a very short time.

Ultimate Consequences for Japan Itself

· Military Defeat and Occupation: The outcome of the war is unquestionable; Japan would suffer a defeat even more devastating than at the end of WWII. Post-war, its national sovereignty would be subject to the strictest limitations. · Regime Change and Demilitarization: The victorious powers and the international community would highly likely compel Japan to undergo “regime transformation,” completely abolishing its existing military forces and potentially implementing long-term international military occupation and supervision to ensure it never again becomes a threat. · Complete Loss of National Status: Japan would fall from being a major global economy and a respected nation to a “rogue state” spurned by the international community and strictly monitored. Its international status and national dignity would suffer a devastating blow, and recovery could take centuries.

In summary, the probability of this hypothetical scenario occurring in reality is extremely low, as Japan’s political elites and citizens are fully aware of its catastrophic consequences. It would be tantamount to national suicide. No rational Japanese leader would or could make such a decision. The answer to this question clearly reveals that the power structure and red lines established based on the outcome of WWII in current international politics remain effective and possess strong deterrent power.

Video: Japan Has Three Profitable Industries Left: Automobiles (rapidly declining), Tourism (rapidly deteriorating), and 🐓 (rapidly booming) 日本只剩下三個賺錢的行業:汽車業(迅速衰落)、旅遊業(迅速惡化)和賣淫業(迅速蓬勃發展)

China–US-Russia Set the Tone! China Launches a Strategic Counterattack! Is Japan Really Ready for This War? 中美俄三方定調!中國陽謀大反擊!日本真要打這一仗?

📅 Highlights of This Episode: Just today, the global landscape took a shocking turn! Well-known commentator “Beiping Feng” offers an in-depth analysis of the latest China–U.S. presidential call. A seemingly casual remark from Trump actually amounted to a direct denial of Japan’s postwar political status!

Facing continuous provocations from Japan’s right-wing forces, China is no longer staying patient. From a “dimensionality-reduction strike” in diplomacy to a thunderous 14-day military drill in the Bohai Strait, the tightening “noose” of countermeasures is clearly underway. However, even more painful than geopolitical rivalry is the economic reality inside Japan…

🚗 With the auto industry being overtaken and tourism entering a deep freeze, what is Japan relying on to maintain its prosperity?

📉 Why are so many young Japanese women flooding into the “special entertainment industry”?

📊 Data reveals: as the former industrial empire collapses, Japan’s only remaining “growth point” is shockingly tragic!

This episode takes you through the brutal truth of geopolitics and uncovers the last “fig leaf” covering Japan’s economic collapse!