Technically correct

Technically correct

With the new series of sanctions by the US, one issue has been settled: The neoliberal world of free trade is officially over. The sooner other countries understand this, the better it will be for their people 隨著美國的新一輪制裁,一個問題得到了解決:自由貿易的新自由主義世界正式結束。其他國家越早了解這一點,對其人民就越有利.

Asia Times: US chip ban de facto declaration of war on China?

America’s latest chip war sanctions risk wider conflict in physical and economic spheres By PRABIR PURKAYASTHA OCT29, 2022

The US-China chip war has entered another debilitating phase.

The United States has gambled big in its latest across-the-board sanctions on Chinese companies in the semiconductor industry, believing it can kneecap China and retain its global dominance.

From the slogans of globalization and “free trade” of the neoliberal 1990s, Washington has reverted to the technology-denial regimes that the US and its allies followed during the Cold War. While it might work in the short run to slow down Chinese advances, the cost to the US semiconductor industry of losing China – its biggest market – will have significant consequences in the long run.

In the process, the semiconductor industries of Taiwan and South Korea and equipment manufacturers in Japan and the European Union are likely to become collateral damage. It reminds us again of what former US secretary of state Henry Kissinger once said: “It may be dangerous to be America’s enemy, but to be America’s friend is fatal.”

The purpose of the US sanctions, the second generation of sanctions after the earlier one in August 2021, is to restrict China’s ability to import advanced computing chips, develop and maintain supercomputers, and manufacture advanced semiconductors.

Though the US sanctions are cloaked in military terms – denying China access to technology and products that can help its military – in reality, these sanctions target almost all leading semiconductor players in China and, therefore, its civilian sector as well.

The fiction of “barring military use” is only to provide the fig leaf of a cover under the World Trade Organization (WTO) exceptions on having to provide market access to all WTO members. Most military applications use older-generation chips and not the latest versions.

The specific sanctions imposed by the United States include:

Advanced logic chips required for artificial intelligence and high-performance computing;

Equipment for 16nm logic and other advanced chips such as FinFET and Gate-All-Around;

The latest generations of memory chips: NAND with 128 layers or more and DRAM with 18nm half-pitch.

Specific equipment bans in the rules go even further, including many older technologies as well. For example, one commentator pointed out that the prohibition of tools is so broad that it includes technologies used by IBM in the late 1990s.

The sanctions also encompass any company that uses US technology or products in its supply chain. This is a provision in the US laws: Any company that “touches” the United States while manufacturing its products is automatically brought under the sanctions regime.

It is a unilateral extension of the United States’ national legal jurisdiction and can be used to punish and crush any entity – a company or any other institution – that is directly or indirectly linked to the United States.

Battle for industry dominance

These sanctions are designed completely to decouple the supply chain of the United States and its allies – the European Union and East Asian countries – from China.

In addition to the firms targeted by the latest US sanctions, a further 31 new companies have been included in an “unverified list.” These companies must provide complete information to the US authorities within two months, or else they will be barred as well.

Furthermore, no US citizen or anyone domiciled in the United States can work for companies on the sanctioned or unverified lists, not even to maintain or repair equipment supplied earlier.

China is doubling down on its indigenous chip-making capabilities.

The global semiconductor industry is currently valued at more than US$500 billion and is likely to double in size to $1 trillion by 2030.

According to a report by the Semiconductor Industry Association and Boston Consulting Group in 2020, “Turning the Tide for Semiconductor Manufacturing in the US,” China is expected to account for approximately 40% of the chip industry’s growth by 2030, displacing the United States as the global leader.

This is the immediate trigger for the US sanctions.

Collateral damage

While the above measures are intended to isolate China and limit its growth, there is a downside for the United States and its allies in sanctioning China.

The problem for the United States, and more so for Taiwan and South Korea, is that China is their biggest trading partner. Imposing such sanctions on equipment and chips also means destroying a good part of their market with no prospect of an immediate replacement.

This is true not only for China’s East Asian neighbors but also for equipment manufacturers like the Dutch company ASML, the world’s only supplier of extreme ultraviolet (EUV) lithography machines that produces the latest chips.

For Taiwan and South Korea, China is not only the biggest export destination for their semiconductor industry as well as other industries but also one of their biggest suppliers for a range of products. The forcible separation of China’s supply chain in the semiconductor industry is likely to be accompanied by separation in other sectors as well.

The US companies are also likely to see a big hit to their bottom line, including equipment manufacturers such as Lam Research Corporation, Applied Materials, and KLA Corporation; the electronic design automation (EDA) tools such as Synopsys and Cadence; and advanced chip suppliers like Qualcomm, Nvidia and AMD.

China is the largest destination for all these companies. The problem for the United States is that China is not only the fastest-growing part of the world’s semiconductor industry but also the industry’s biggest market.

So the latest sanctions will cripple not only the Chinese companies on the list but also the US semiconductor firms, drying up a significant source of their profits and, therefore, their future research and development investments.

While some of the resources for investments will come from the US government – for example, the $52.7 billion chip manufacturing subsidy – they do not compare to the losses the US semiconductor industry will suffer as a result of the China sanctions.

This is why the semiconductor industry had suggested narrowly targeted sanctions on China’s defense and security industry, not the sweeping sanctions that the United States has now introduced; a scalpel rather than a hammer.

Technology denial

The process of separating the sanctions regime and the global supply chain is not a new concept.

The United States and its allies had a similar policy during and after the Cold War with the Soviet Union via the Coordinating Committee for Multilateral Export Controls, or COCOM (in 1996, it was replaced by the Wassenaar Arrangement), the Nuclear Suppliers Group, the Missile Control Regime, and other such groups.

Their purpose was very similar to what the United States has now introduced for the semiconductor industry. In essence, they were technology-denial regimes that applied to any country that the United States considered an “enemy,” with its allies following – then as now – what the United States dictated.

The targets on the export-ban list were not only the specific products but also the tools that could be used to manufacture them. Not only the socialist bloc countries but also countries such as India were barred from accessing advanced technology, including supercomputers, advanced materials, and precision machine tools.

Under this policy, critical equipment required for India’s nuclear and space industries was placed under a complete ban.

Though the Wassenaar Arrangement still exists, with countries like even Russia and India within the ambit of this arrangement now, it has no real teeth. The real threat comes from falling out with the US sanctions regime and the US interpretation of its laws superseding international laws, including WTO rules.

China’s trade with the US has boomed through the pandemic.

The advantage the United States and its military allies – in the North Atlantic Treaty Organization, the Southeast Asia Treaty Organization, and the Central Treaty Organization – had before was that the US and its European allies were the biggest manufacturers in the world. The United States also controlled West Asia’s oil and gas, a vital resource for all economic activities.

The current chip war is being waged at a time when China has become the biggest manufacturing hub of the world and the largest trade partner for 70% of countries in the world. With the Organization of the Petroleum Exporting Countries no longer obeying Washington’s diktats, the US has lost control of the global energy market.

Why now?

So why has the United States started a chip war against China at a time that its ability to win such a war is limited? It can, at best, postpone China’s rise as a global peer military power and the world’s biggest economy.

An explanation lies in what some military historians call the “Thucydides trap”: When a rising power rivals a dominant military power, most such cases lead to war. According to the Athenian historian Thucydides, Athens’ rise led Sparta, the then-dominant military power, to go to war against it, in the process destroying both city-states; therefore, the trap.

While such claims have been disputed by other historians, when a dominant military power confronts a rising one, it does increase the chance of either a physical or economic war. If the Thucydides trap between China and the United States restricts itself to only an economic war – the chip war – we should consider ourselves lucky.

With the new series of sanctions by the United States, one issue has been settled: The neoliberal world of free trade is officially over. The sooner other countries understand this, the better it will be for their people.

And self-reliance means not simply the fake self-reliance of supporting local manufacturing, but instead means developing the technology and knowledge to sustain and grow it.

This article was produced in partnership by Newsclick and Globetrotter, which provided it to Asia Times.

Prabir Purkayastha is the founding editor of Newsclick.in, a digital media platform. He is an activist for science and the free software movement.

US Trade Representative Katherine Tai said China must made changes to be like US. To be a failed state like US? No wonder most of the non-AngloSaxon nations not a US colony wants to share China’s common prosperity for mankind, not US’s miseries. 美國貿易代表戴琪説中國必須做出改變,要變成像美國一樣。像美國這樣的失敗國家?難怪大多數今天還沒有被美國殖民的非白人國家願意加入分享中國的人類命運共同體, 而不是美國的大小通吃的損人利己的政策.

Video: When is TSMC final curtain? What is left for Taiwan after US destroyed TSMC? 台積電的結局 被美吸星大法吞噬後

https://rumble.com/v1qgvsa-when-is-tsmc-final-curtain-what-is-left-for-taiwan-after-us-destroyed-tsmc.html

https://m.facebook.com/story.php?story_fbid=822053422351318&id=100036400039778

During the 2019 US’s NED backed terrorists attacked HK police, LEGCO Members and their families, Nancy Palosi not only voiced support, said what a beautiful sight. Karma comes home (her home) like a high speed train. 在 2019 年美國民主基金會支持的恐怖分子襲擊香港警察、香港立法會議員及其家人期時Nancy Palosi 不僅表達了支持,還稱這是一個美麗的風景線, 報應就像高速列車一樣跑到她的家𥚃.

The 0-3 quarantine requirements bad for business so far attracts only 10% visitors to HK, many of the businesses executives I have spoken to said unless HK matching Singapore’s 0-0 they have no plan to go to HK. I am a member of HKANC and former President of HKBAH, members I have spoken to most are not going to the HK forum with 0-3 that I and and others help found when I was President of HKBAH (see picture). Even before the pandemic, HK Forum no longer received the support from HKCE like before!

France Protest Video: President Macron Pledges to Solve the Crisis, but difficult since France is a US Colony 法國抗議現場視頻: 馬克龍總統承諾解決危機, 但困難重重, 因為法國是美國殖民地

https://rumble.com/v1qdok8-president-macron-pledges-to-solve-the-crisis-but-difficult-since-france-is-.html

https://m.facebook.com/story.php?story_fbid=821584279064899&id=100036400039778

Russia-Ukraine War : Members of the French far-left trade union retook the streets & protested against the highest inflation. They marched through the streets of Paris with slogans & banners. The Protestors are demanding pay rises to compensate for inflation. Currently. France is facing a ‘Cost of Living Crisis’. Last week workers of trade union ended nearly a monthlong strike over pay hikes. Is this the beginning of the brewing revolution in France?

Fictional imaginary countries and place not appeared on United Nation country’s list 這些虛構的國家和地點護照未出現在聯合國國家名單上

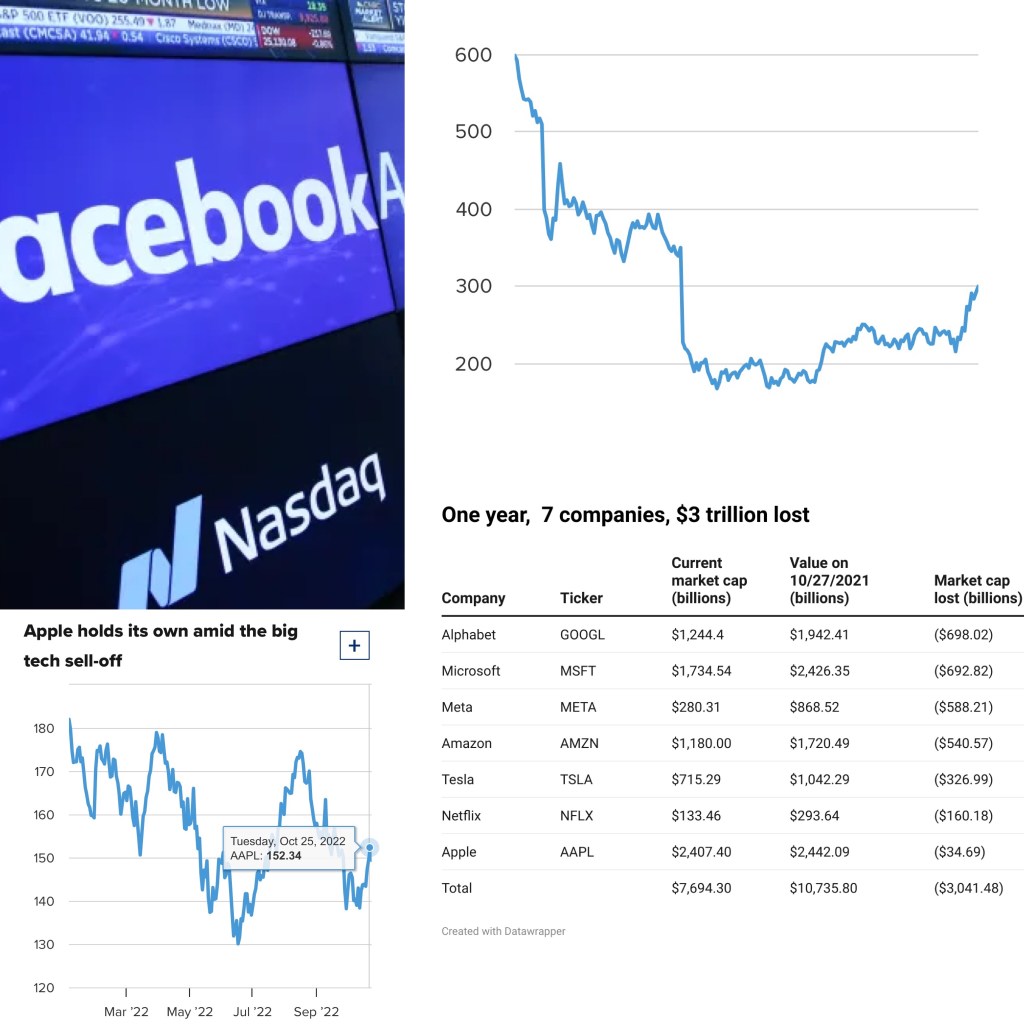

Biden tech war against China cost tech companies US$3 trillions loss in 1 year and increasing, their share prices crashing 拜登針對中國的科技戰爭使科技公司在一年內損失了 3 萬億美元,而且還在不斷增加,它們的股價暴跌 by KJ, SF Bay Area China Group 10-28-22

https://www.statista.com/chart/28581/big-tech-market-capitalization/

Silly Reuters can’t name the Elephant in the room: Tech war against China

Their disappointing results suggest that even the strongest U.S. companies are feeling the effects of tighter Fed policy, a soaring dollar and persistent inflation.

The Financial industry is also at risk: Credit Suisse in danger:

https://www.nakedcapitalism.com/2022/10/its-time-to-worry-about-the-health-of-another-too-big-to-fail-european-bank.html

This is an interesting article analysing why China’s tech succeeded while the US’s is sunsetting: Neoliberal financialization for shareholder profits rather than research/investment/development, turning US/Western tech giants into financial corporations with an IT department: The US corporations ate their own seed corn. The CHIPS act will not turn that around.

While through the process of indigenous innovation, Chinese companies have become major global competitors, many US technology companies have fallen victim to corporate financialization. The starkest contrast is between the success of Huawei Technologies in communication infrastructure, in which the company is the world leader (followed by Sweden’s Ericsson and Finland’s Nokia), and the failure of US-based Cisco Systems to become a significant competitor in this segment. In a forthcoming paper, “The Pursuit of Shareholder Value: Cisco’s Transformation from Innovation to Financialization,” Marie Carpenter and William Lazonick document how, at the turn of this century, Cisco was positioned technologically to build on its global leadership in enterprise networking equipment to become a major competitor in the more sophisticated service-provider infrastructure segment. To do so, Cisco would have had to make large-scale investments in manufacturing and marketing as well as R&D. Instead, from 2002-2021, Cisco distributed USD144 billion (98 percent of net income) to shareholders in the form of stock buybacks as well as USD48 billion (another 33 percent of net income) as dividends. More generally, corporate financialization has robbed the United States of the possibility of attaining a leadership position in 5G and IoT.

In smartphone competition with Huawei, Apple has benefited immensely from US trade policy that, from the fourth quarter of 2020, eviscerated the Chinese company’s high-end smartphone output by coercing TSMC to stop shipping advanced nanometer chips to HiSilicon, Huawei’s chip-design subsidiary. Yet TSMC’s rise to global dominance of advanced chip fabrication was enabled by the fact that Apple itself chose to outsource semiconductor fabrication while, between October 2012 and June 2022, wasting USD529 billion on stock buybacks (92 percent of net income) to give manipulative boosts to its stock price. Apple could have deployed just a fraction of this cash to fund on a sustained basis its own state-of-the-art fab—as indeed an industrial journalist suggested to Apple CEO Steve Jobs in 2010. To put the extent of this corporate financialization in perspective, the combined USD27 billion that TSMC and Samsung Electronics committed to spending over several years from 2021 to launch state-of-the-art fabs in the United States was less than one-third of the USD86 billion that Apple spent on buybacks in 2021 alone.

Meanwhile, as has explicitly been recognized by Pat Gelsinger, Intel’s CEO, who took office in February 2021, corporate financialization has been a prime cause of that company’s loss of world leadership in chip fabrication to TSMC and Samsung. China’s SMIC may be struggling to catch up with the Taiwanese and Korean companies in advanced nanometer platforms, but Intel’s financialization has helped create an opening for SMIC’s development path. The same argument can be made about how Boeing’s corporate financialization, manifested by USD43 billion in buybacks from January 2013 to the first week of March 2019, just before the second of the two Boeing 737 MAX crashes, crippled a US-based technology leader, enhancing the possibility that China’s Comac, with its C919, might break into the Boeing-Airbus duopoly in the global manufacture of large aircraft.

Video: The Apocalypse of the Russian-Ukrainian War, US, NATO & EU failed to crush Russia. EU biggest losers! Who is the real military power between China, the United States and Russia? 俄烏戰爭啟示錄 美國、北約和歐盟未能粉碎俄羅斯, 歐盟被美國出賣, 中美俄 誰是真正軍事大國?

https://rumble.com/v1qbuh2-who-is-the-real-military-power-between-china-the-united-states-and-russia.html

https://m.facebook.com/story.php?story_fbid=821372709086056&id=100036400039778