Asia Times: New Commerce Department chip and equipment bans against China are hitting US semiconductor company shares hardest. 亞洲時報:商務部對中國的新芯片和設備禁令對美國半導體公司股票的打擊最大. By Scott Foster, Oct 17 2022

On October 7, the US Department of Commerce expanded licensing requirements for exports of advanced semiconductors and the equipment that’s used to make them to cover all shipments to China and not just shipments to particular companies.

The share prices of companies expected to be affected had already dropped, discounting previously announced sanctions and the downturn in the semiconductor cycle that was already underway.

From their 52-week highs to recent 52-week lows:

Intel (INTC) was down 56%;

Micron (MU) was down 50%;

Nvidia (NVDA) was down 69% (its products having been directly targeted by the Biden administration); and

AMD (AMD) (also directly targeted) was down 67%.

Among US semiconductor equipment companies:

Applied Materials (AMAT) was down 57%;

Lam Research (LRCX) was down 59%; and

KLA (KLAC) was down 45%.

Outside the United States, ASML (ASML) of the Netherlands was down 59% from 52-week high to 52-week low. Japanese equipment makers Tokyo Electron (TYO 8035) and Screen Holdings (TYO 7735) were down 50% and 44%, respectively.

Japanese semiconductor makers Renesas (TYO 5723) and Rohm (TYO 6963) were down only 27% and 28%, but they focus on automotive and industrial semiconductors, not the artificial intelligence and high-performance computing devices that obsess the Biden administration. Their 52-week lows were last March.

SMIC (HKG 0981), China’s top IC foundry, was down 40% while TSMC (TPE 2330) was down 43% – a relatively strong performance under the circumstances.

In terms of share price performance and investor returns, American companies and ASML have been hit harder than the Chinese. That might seem ironic considering the measures target China, but it is the market’s discounting mechanism at work.

US government policy is aggravating what was already shaping up to be a severe industry downturn – and friendly fire is a real problem.

On its earnings call on October 13, TSMC announced that it had decided to reduce 2022 capital spending to US$36 billion from about $40 billion due to falling global demand for semiconductors and rising costs.

Management had planned to spend $40 billion to $44 billion this year but said in July that actual spending would be at the bottom of that range. Compared with the $30 billion spent in 2021, projected growth has dropped from a maximum of 47% to 33% and is now 20%.

Mitigating factors for TSMC include a one-year authorization from the US government to continue with the expansion of its facilities in Nanjing and the possibility of a rebound in demand when China’s Covid restrictions are loosened. But TSMC CEO C C Wei also told the media that “We expect probably in 2023 the semiconductor industry will likely decline.”

At the end of September – when announcing results for its fiscal year 2022, which ended on September 1 – US memory chip maker Micron told investors that the company’s capital spending would be cut by a third, from $12 billion to about $8 billion, in the year ahead.

Construction spending should more than double, “to support demand for” the second half of the decade, “but spending on wafer fab production equipment is likely to decline by nearly 50% due to “a much slower ramp of our 1-beta DRAM and 232 layer NAND [the company’s newest and most advanced products] versus prior expectations.”

Furthermore, “To immediately address our inventory situation and reduce supply growth, we are selectively reducing utilization in both DRAM and NAND.” Reports from Micron and its South Korean and Japanese competitors indicate that memory chip production has been cut by about 30%.

Samsung’s approach to capital spending is similar to Micron’s. Its “shell first” strategy is to build clean rooms first so it can install equipment flexibly and rapidly when the time comes. On October 4, Samsung announced plans to launch a 2-nanometer foundry process (matching TSMC) by 2025 and a 1.4-nanometer process by 2027.

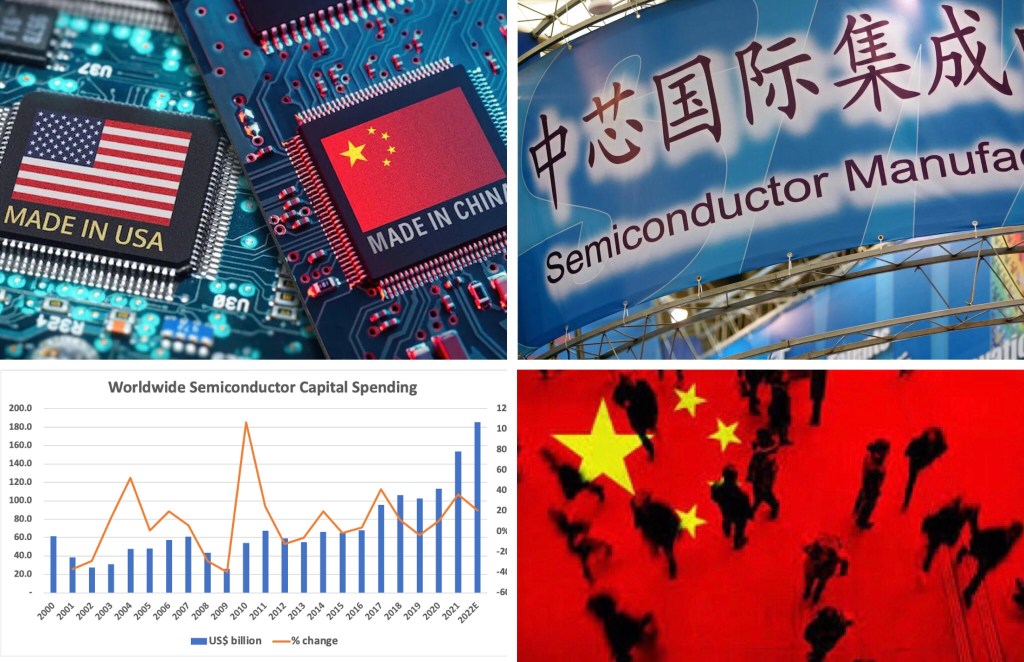

As the global economy weakens and US high-end decoupling from China accelerates, the outlook for semiconductor capital spending continues to deteriorate. Last March, market research organization IC Insights forecast a 23.5% increase to $190 billion in calendar 2022.

That industry capital spending figure was reduced to $185.5 billion in August but the announcements from TSMC and Micron point to a sharper decline. Handel Jones, CEO of American consulting firm International Business Strategies, estimates the figure at $160 billion, an increase of only 4% over last year’s $153.9 billion.

IC Insights itself qualified its August forecast, writing that “a menacing cloud of uncertainty looms on the horizon. Soaring inflation and a rapidly decelerating worldwide economy caused semiconductor manufacturers to re-evaluate their aggressive expansion plans at the midpoint of the year. Several (but not all) suppliers – particularly many leading DRAM and flash memory manufacturers – have already announced reductions in their capex budgets for this year.

“Many more suppliers have noted that capital spending cuts are expected in 2023 as the industry digests three years of robust spending and evaluates capacity needs in the face of slowing economic growth.”

When the dot.com bubble burst in 2000, semiconductor capital spending dropped 55% in two years. The Lehman Shock triggered a 57% decline, also over two years. Now, capital expenditure is dropping back from an all-time record high, suggesting a decline of similar magnitude and perhaps duration.

On October 12, The Wall Street Journal reported that US equipment makers including KLA and Lam Research have halted installation and support of equipment at China’s Yangtze Memory Technologies Co (YMTC) while assessing the new US Commerce Department rules. The share price of Japanese NAND flash memory maker Toshiba (TYO 6502), which competes with YMTC, jumped 10% on the news.

YMTC’s NAND flash memory is good enough for Apple and there is no evidence that its technology was stolen, so this can be considered an escalation of US policy from the punishment of bad actors to an all-out attempt to stifle Chinese artificial intelligence (AI) and high-performance computing and thus roll back the development of China’s economy.

Commencing immediately, the withdrawal of American support staff will crimp Chinese semiconductor production.

In addition, a new Commerce Department regulation that “restricts the ability of US persons to support the development, or production, of ICs at certain PRC-located semiconductor fabrication ‘facilities’ without a license” is already disrupting the operations of Chinese companies.

By forcing numerous executives and engineers of Chinese extraction to choose sides, it brings decoupling down to the personal level.

Data from Tokyo Electron show the company’s total sales of semiconductor production equipment up 2.6 times in the five years to March 2022 (the company’s fiscal year ends in March). The increase was led by a 5.7x increase in China, which grew from 12% to 26% of total sales.

In the two years to March 2022 alone, sales in China increased by 2.7x. That suggests that the Chinese semiconductor industry has purchased enough equipment to see it through the next two or three years, at least.

Tokyo Electron’s performance in other regional markets was not exceptional. Sales were up 2.7x in Korea, 2.6x in the US, 2.5x in Japan, 1.8x in Europe, 1.6x in Taiwan (which started at a high level), and 2.1x in Southeast Asia and other regions.

As Japan’s largest and the world’s third-largest maker of semiconductor production equipment, with a diversified product portfolio, Tokyo Electron is representative of the industry as a whole.

The Chinese can no longer rely on US equipment suppliers and European and Japanese suppliers must follow US rules if their products incorporate US technology, so China will step up its import substitution campaign.

Sanctions on China have already caused large losses for American semiconductor and equipment companies, and more are probably on the way. Furthermore, in the next up-cycle, the China opportunity for foreign suppliers is likely to be much diminished.

Follow this writer on Twitter: @ScottFo83517667